Corpotate tax and Changes in Income Tax rules – Diligent IAS 22/09/2019 – Posted in: Daily News

CHANGES IN TAX RULES

For: Mains

Topics covered:

- Changes in Corporate tax and Income tax rules

News Flash

In order to revive the private investment and lifting growth, the FinMin announced big cuts in the corporate tax rate.

- The government rolled back enhanced surcharge on capital gains arising on sale of equity share in a company or a unit of an equity-oriented mutual fund in the hands of an individual.

Changes in Income Tax Act

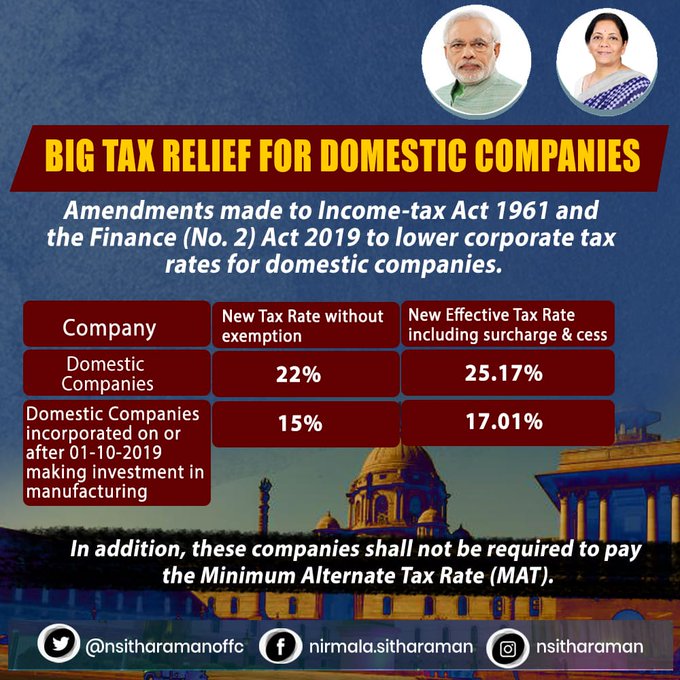

- The government slashed basic corporate rate tax to 22% from 30% for domestic companies that don’t avail any exemption/incentive.

- The effective tax rate for these companies shall be 25.17% inclusive of surcharge and cess. Also, such companies shall not be required to pay Minimum Alternate Tax or MAT.

- The government has slashed corporate tax rate to 15%, from 25%, for domestic companies incorporated on or after 1st October 2019 making fresh investment in manufacturing.

- The option to pay income tax at the rate of 15% is available to companies which do not avail any exemption/incentive and commence their production on or before 31st March, 2023.

- The effective tax rate for these companies shall be 17.01% inclusive of surcharge & cess. Also, such companies shall not be required to pay Minimum Alternate Tax.

- A company which does not opt for the concessional tax regime and avails the tax exemption/incentive can continue to pay tax at the pre-amended rate. After expiry of their tax holiday/exemption period, these companies can opt for the new concessional tax regime.

- The government has reduced the rate of Minimum Alternate Tax or MAT to 15%, from 18.5%.

- The government rolled back increased surcharge introduced in this year’s Budget on capital gains arising on sale of equity share in a company or a unit of an equity oriented fund or a unit of a business trust liable for securities transaction tax, in the hands of an individual, HUF, AOP (Association of Persons), BOI (Body of Individuals) and AJP (Artificial Juridical Person).

- The enhanced surcharge will also not apply to capital gains arising on sale of any security including derivatives, in the hands of Foreign Portfolio Investors (FPIs).

- To provide relief to listed companies that had announced share buyback before 5th July 2019, the government exempted such companies from buyback tax announced in the Budget.

Source: Livemint

READ MORE DAILY NEWS

- Train-the-trainer Programme in Artificial Intelligence

- NGOs will fall under the Right to Information Act

- Two new plant species discovered

- National Centre for Clean Coal Research and Development

You are on the Best Online IAS preparation platform. You are learning under experts.

We are present on Facebook- Diligent IAS, LinkedIn- Diligent IAS, YouTube- Diligent IAS, Instagram- Diligent IAS. Get in touch with us.